CBSL policy rates up by 700 bps; Acquest recommends further exposure to Real Estate

Market sector

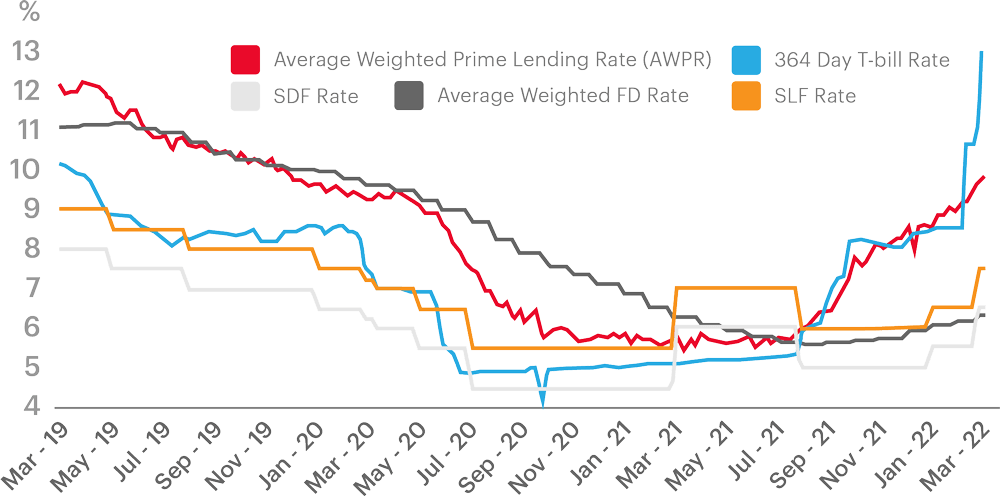

Historically, the Average Prime lending rate (AWPLR- indicative of the spot interest rates o ered to prime customers of banks) has adjusted fast to the changes in policy rates. CBSL 364 day T-bill rates adjust before policy rate changes while deposit rates has noticeable time lag.

Market lending rates will increase further and bank lending rates are expected to double

Government T-bill rates have already started moving upwards since August 2021 to reach 15.69% as at 31st March 2022. Bank lending rates are expected to double within a short period of time in response to the policy rate hike.

Deposit rates to reach double digit territory during medium term

Deposit rates will take some time to adjust to the full extent of the hike. Further, FD rates which are determined by credit demand will probably require CBSL to urge the banking sector to adopt the indicated FD rates. If at least one state bank or any other Licensed Commercial Bank (LCB) adopts these rates other banks will have to follow.

High interest rates to limit credit growth

With the significant rise in market interest rates, demand for credit will come down mainly due to reduced consumption and reduced investments as businesses reduce expansion. This would increase savings. There will be high competition among banks and Non Banking Financial Institutions (NBFIs) as diversification becomes limited with low credit demand.

Reduced consumption & liquidity to ease the inflationary pressure

to some extent

Short-term future inflation is determined by the present market behavior; hence we expect inflation to come in elevated levels in the upcoming months. Further, Sri Lanka is a net importing country with essentials such as fuel, food items and medicine dominating the import bill. Due to the increase in price of these in world markets and the LKR depreciation (55% YTD) cost push inflation will prevail. However, the sharp interest rate hike helps in reducing liquidity in the market as well as curtailing consumption, which will ease the inflationary pressure to some extent. We also expect high interest rates to bring a certain level of stability to the depreciating LKR in the short to medium term.

Return on investment of equity to slow down

Going forward, the profitability growth of listed companies will be limited due to low economic activity, high interest charges and high tax charges. In addition, an increase in margin trading costs will drive the cost of investment in equity securities. Both of the above will lead to a reduction in net gains for investors.

Low real returns from fixed income assets due to high inflation

Although fixed income instruments provide higher returns, considering the high inflation supported by the depreciating LKR, it would still provide negative overall real returns.

Real estate sector to be resilient despite reduced economic activities

Low leverage in this asset class will support preserving real estate values

The residential real estate sector is mostly equity-funded with very low borrowings involved to purchase real estate assets. This is further supported by housing-related loans contributing less than 10% of the total loan portfolio of selected Licensed Commercial Banks (state-owned & privately owned) and larger NBFIs. Having low exposure to bank borrowings would contribute to less sensitivity to interest rates; thus, we feel real estate returns improve in the medium to long term.

Condominium Market

- High interest rates and a significant rise in the cost of construction will curtail future supply.

- The high cost of construction will deter construction of houses and will increase demand for completed apartments.

- Completed or almost completed condominiums (existing inventory) are already repricing to USD. Demand for apartments will go up as investors look to these properties to diversify LKR risk.

- The above factors are further strengthened by 100% YOY growth in condominium property volume index in 2021 Q4.

Modern housing Cost Index

Colombo Land & Housing

- Scarcity of prime residential land in central Colombo will continue to see demand from end users and large investors looking to preserve their wealth. As we see demand outweighing supply, we expect significant price appreciation in the short to medium term.

- Land prices will reprice in relation to apartment prices in the premium segment in the medium term.

Suburban Land & Housing

- Based on Acquest’s internal analysis, we found that mispriced assets are present in suburbs which will provide opportunities for value gains

Villas, Beachfront/Waterfront Properties

- Villas and beachfront properties are priced in USD and there is limited supply in this segment.

- We expect prices in this segment to remain dollarized and the demand from foreign investors to increase.

Commercial Property

- Term loans which are collateralized with commercial property, contribute largely to the loan portfolio of banks.

- Rise in interest rates will increase non-performing loans within “term loan” category, creating an opportunity for bargain purchase at auctions of foreclosed property.